Being able to manage our money is one key to survival. Currently I happened to talk about someone who seems to be bad at managing money. I’m going to use “they” to refer to the person because I do not want to reveal the “gender” as a “giveaway”. I actually feel sorry for them but seeing their lifestyle somehow makes feel desperate. Like, you cannot keep eating out if you know you will have no money to eat at the end of the month. You cannot go shopping for something you don’t need simply because you want it when you know you’ll need the money to survive later. And this person does just that. They love eating out. They love shopping. And at the end, they have no money.

Well, I don’t mean to judge. But financial management is important to me. I was poor; I knew how it felt to have no money and no one to help, so yes, I feel obliged to help those having no money, but you know, that’s not the issue I want to talk about here. I want to talk about managing our money, how to survive! My mom has taught me that I must save, just in case. So here is what I do: When I buy something, I don’t think of how much money I still have left. Instead, I think of how much money I’ve spent and how much money I’ll have to spend to limit the amount I can spend. First, I look at how much money I receive. Then I’ll count how much I’ll spend for my apt rent, electricity bills, phone provider, etc. (basically the basics). Then I’ll count how much I want to save (so I can travel, etc. :D) Then I calculate how much I can spend. If I feel that I have too much to spend I’ll take some of it and put it into my “emergency saving”. So let’s say I get $1000 per month. Then my apt, electricity, phone, etc. costs $550 (1); I still have $450. Then I want to save at least $150. It means I have $300 left to spend for one month. But I think $300 is too much, so I put $100 into “emergency savings”; it means I have only $200 to spend for “shopping” (including grocery shopping!). Hence, every time I go shopping, I refer my money to these $200 and $100, not the $1000 I receive, not the $450 after the $550 basic expense. When I shop, eat out, hang out, etc., this is what I think: “Ok, I’ve spent $150, it means I still have $50, I still have one week left this month, so I must not spend it all today. Etc.” This kind of thinking will make me really think about whether to buy something or not on the basis, “Do I really need this?” and not simply, “Do I want this?” And in the occasion where I’ve spent all $200, but I need to spend more money (something like suddenly I need to buy something for my group project, etc.) or because I really want something and am worried that it will be out of stock if I should wait for the next month (ha!) then I use the other $100. And if I still have some left, then it goes to the saving. If I only spend $50 from my emergency saving, for example, then I have it go to the general monthly saving and sometimes the next month I refer to it thinking, “Oh, I still have $50 left from last month, so shall I want to spoil myself, I can spend extra.” But of course the next month I try not to spend more than the $200 that I’ve set to spend.

With this scenario, one thing is for sure: I secure at least $150 per month. And sometimes I can save more than $150. But after I save the monthly $150, I’ll “forget” it and does not count it as my money to spend. However, I accumulate my emergency saving; you know, the money that is left from my $100 monthly emergency saving. Well, because we’ll never know what will happen. Sometimes the money is late. Sometimes I simply don’t get as much, etc. Thus, I want to feel at ease knowing that if the bad happens, I can still survive because I have saved; I don’t have to worry about what I should do if the bad thing happens tomorrow because I’ve spent all my money today.

Well, some people would tell me that I should have fun too and get what I want. “Don’t be too stingy with yourself” they say. Well, I understand. But life is not only about having fun but also how to survive. I save so that when I have no income, I don’t have to bother others about it because I’ve anticipated it. I’m not that good of a person, like, I can’t help everyone, so the least I can do is not to bother them so they don’t need to help me, so they can help themselves.

Yeah I know that we don’t take our money with us when we’re dead. But when I am dead, I’ll still need money to take care of my corpse, my burial, etc., right? And if I still have money left by the time I’m dead, it can be used for or by those who are still alive, who need it. I have no regret. “But you didn’t get to enjoy the money you earn by your hard work?” They say. Well, I have, as necessary. I save for what I need in case tomorrow I’m still alive.

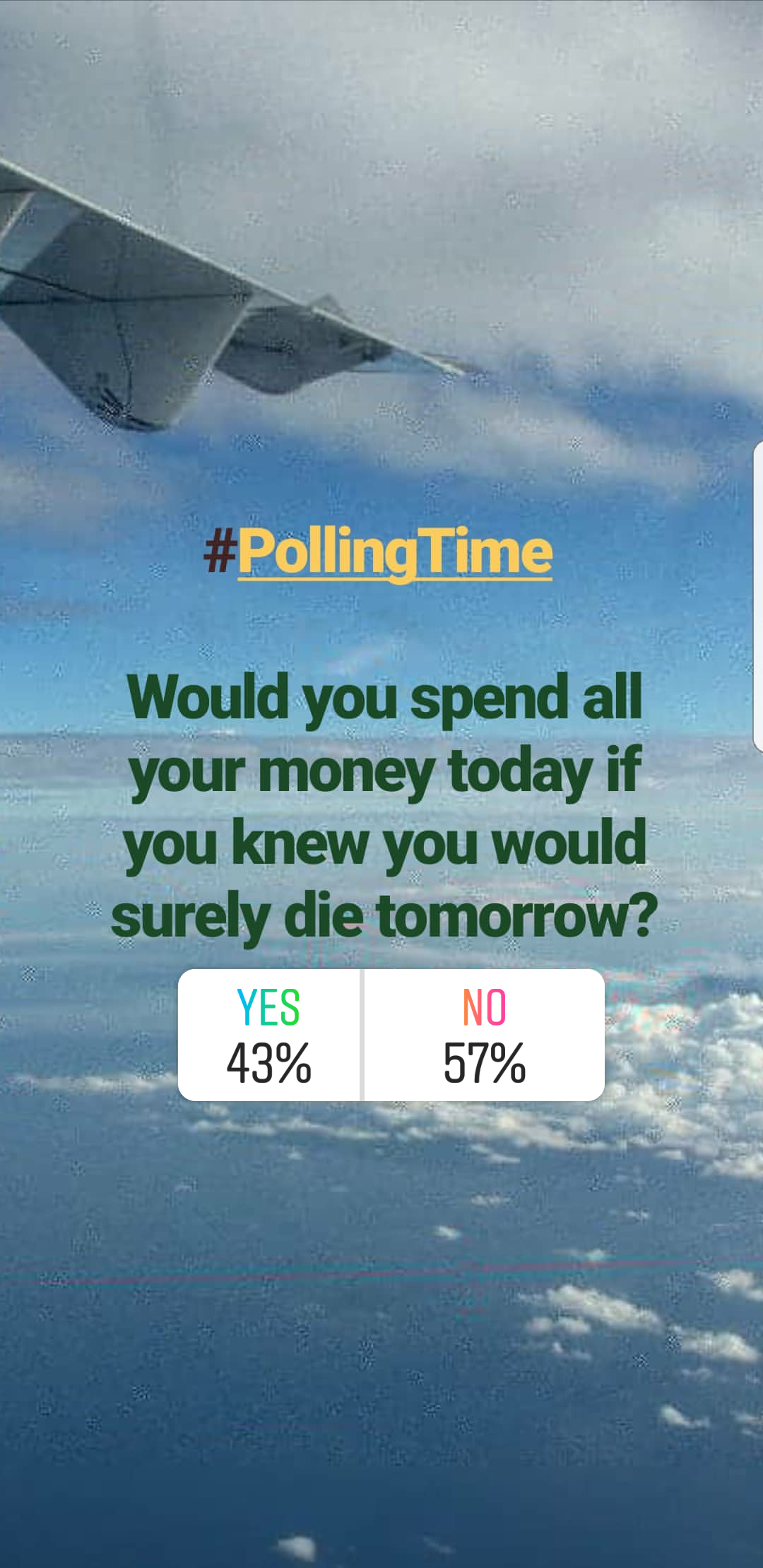

Besides, I’d rather die tomorrow and have some money left than spend all my money today and live tomorrow with nothing left, because, well, we don’t know if we’re still going to live or die tomorrow, right?

A poll I made on my Instagram stories.

And by the way, here is a conversation with a friend from sometime ago that I posted on my Instagram about financial management:

…

B: What about your scholarship? Do you get the money every month?

A: No, I get the money once every 3 months.

B: Wow. So you’ve got a lot in the beginning?

A: Kinda. But I have to manage it well so I can survive all the three months.

B: But how can you resist it?

A: Resist what?

B: You know, not spending your money in the beginning, when you receive it. When it looks a lot.

A: Mmm, maybe because I wasn’t born rich. I mean, I didn’t grow up in a rich family. My parents were not public officers or employees with monthly fixed salary. Sometimes we got none. Sometimes we got a little. Sometimes we got more. But I can say we didn’t really have any “issue” with money because we just made do with the little amount we had. Or maybe because we don’t like complaining about it. Basically we live and buy things based on what we need. Living with no money sucks. My Mom always tells me to save when I get more money, because we never know when we won’t be getting any. So when we got more, we saved and forgot it, pretending that we had no savings. When we got none, somehow we could use the saving for our needs. I remember often wanting sth and Mom would not buy it for me because she thought I didn’t or wouldn’t need it, basically because we ‘had no money for it’. When my friends were wearing brand new stuff, Mom bought me used clothes with much lower prices, sometimes even too big of a size so I could wear them for years. As a kid, I might have pouted or resented it. But now I am thankful. It teaches me to set my priority especially when things are limited. And hey, I want to travel. I need to save!

B: But you can always borrow, from friends, from family…

A: Ah, it’s never really been an option. We were poor. If we borrowed some money when we had none, there was never a guarantee that we would be able to pay back. So it’s better to stay out of it. As in not having debts, you know. Some people thought we were rich, well, maybe we were, because being rich is not just about having a lot of money, I guess. It’s being able to survive when you have ‘none’. And we did survive.

.

Now if you wonder why I am not impressed with guys boasting or spending their (parents’) money lavishly, you know why. It’s easy to live with a lot of money. But it’s not as easy when you have none. (And there’s no guarantee those guys will be okay when they run out of money 😛).

[…] there, a long time ago I wrote about how to survive and manage our money. You can read it here. It’s more about how we should allocate our money when we get money/salary, though. This time […]